E - PAPER

CURRENT MONTH

LAST MONTH

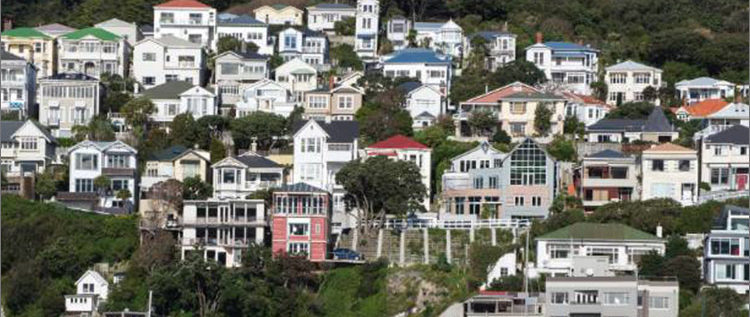

New Zealand Reserve Bank Mortgage-lending Rules to Tackle Housing Crisis

New Zealand’s reserve bank has announced plans to tighten up mortgage-lending, as the country struggles to tackle its housing crisis. One measure, which would come into force from 1 October after consultations, will involve reducing the portion of loans banks can make

BY

Realty Plus

BY

Realty Plus

Published - Wednesday, 04 Aug, 2021

New Zealand’s reserve bank has announced plans to tighten up mortgage-lending, as the country struggles to tackle its housing crisis. One measure, which would come into force from 1 October after consultations, will involve reducing the portion of loans banks can make to owner occupiers with less than 20% of their deposit.

In October the bank will also begin consulting on implementing debt-to-income (DTI) restrictions and interest rate floors to make sure that borrowers can afford to service their mortgages. “We are focused on ensuring borrowers are resilient to a range of future economic and financial conditions. We are particularly concerned about those who have borrowed in the past 12 months at high LVRs (loan-to-value ratios) and high DTIs. If house prices were to fall, some buyers could face the possibility of negative equity – which means the value of their property is below the outstanding balance on their mortgage,” reserve bank deputy governor Geoff Bascand stated.

House prices have rocketed in New Zealand over the past decade, with asking prices up by 20% in June compared to the same month last year, according to one recent report. Existing problems with affordability, high costs of materials and regulations constraining urban supply have been compounded by ultra-low interest rates, and a faster-than-expected economic recovery from the pandemic.

The finance minister, Grant Robertson said, “The bank should make sure the changes did not unduly impact first homebuyers. The government has already put in place a number of measures to cool the housing market to make house prices more sustainable and tilt the balance in favour of first homebuyers, including extending the bright-line test and removal of interest deductibility.”

RELATED STORY VIEW MORE

Nigeria Shows Widening Transparency Gap in Real Estate

Singapore Private Home Rents Set To Climb By 10-15%

Saudi Arabia’s Ambitious Projects from World’s Largest Airport to Skyscraper

NEWS LETTER

Subscribe for our news letter

E - PAPER

-

CURRENT MONTH

LAST MONTH

REALTY+ SPECIAL ISSUES

Test Magazine

THE TECH TITANS 2022

COFFEE TABLE BOOK 2022

Anniversary Issue 2022

Anniversary Issue 2020

VIDEO GALLERY VIEW MORE